Introduction

Introduction

Universal Health Coverage (UHC), as defined in Sustainable Development Goal (SDG) 3.8, entails access to essential health services of sufficient quality without exposure to financial hardship. Bangladesh has achieved notable health improvements over past few decades. But these gains are still being undermined by the financing system which is dominated by out-of-pocket (OOP) expenditure. This structure perpetuates inequity, financial risk and limits system resilience.

As Bangladesh prepares for graduation from Least Development Country (LDC) status on November 24, 2026. This milestone marks substantial gains in income, human resources and economic resilience. However, it may strain the country’s progress in SDG 3 and related health outcomes due to the loss of trade preferences and tightened intellectual property provisions that could increase medicine prices, and reduce access to concessional international resources. Therefore, strengthening health financing through risk pooling instruments such as health insurance is key to UHC, as well as to maintaining health achievements and a smooth transition out of Bangladesh’s LDC status.

Persistent Health Inequities

The Bangladesh Demographic and Health Surveys (BDHS) data reveal significant inequalities in maternal health service utilization among the people of different socio-economic backgrounds, such as in terms of their wealth and residence. For example, while 82% of women had at least one antenatal care (ANC) visit, only 37–46% had four or more visits as per BDHS 2017-18.By 2022, the proportion of pregnant mothers’ at least one ANC visit increased to 88%; but four or more ANC visits decreased to around 41%.

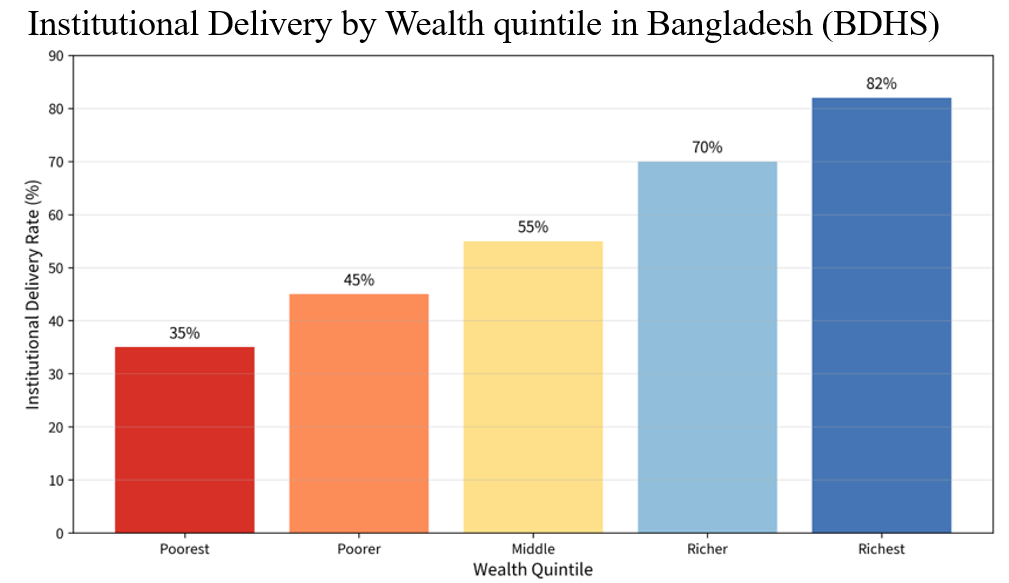

Institutional delivery rates are more unequal. The highest rates are between 70–80% in the richest quintile and 33–42% in the poorest quintile. The coverage is 66-76% in urban areas and 48-60% in rural areas. This is the same with skilled birth attendance. These disparities are due to financial and structural barriers. Poorer and rural households have high direct costs (consultation fees, medicines, transport) and indirect costs (e.g., lost wages) resulting in delayed care and a fragmented health system.

Institutional delivery rates are more unequal. The highest rates are between 70–80% in the richest quintile and 33–42% in the poorest quintile. The coverage is 66-76% in urban areas and 48-60% in rural areas. This is the same with skilled birth attendance. These disparities are due to financial and structural barriers. Poorer and rural households have high direct costs (consultation fees, medicines, transport) and indirect costs (e.g., lost wages) resulting in delayed care and a fragmented health system.

Preventive care gap and NCD burden

Low rates of completing recommended ANC packages reflect wider gaps in the provision of preventive services.This deficit is also growing more and more problematic in the context of the growing burden of non-communicable diseases (NCDs).BDHS 2017-18 showed that the prevalence of hypertension among adults (18 years and above) was about 27% and diabetes was about 10%.Further increases are revealed in more recent analyses of BDHS 2022 data, with a significant increase in the prevalence rates (e.g., up to 16–49% across specific adult age groups depending on measurement and analysis).

Early screening and management have significant advantages. Screening programmes for hypertension, diabetes, cancers (such as cervical, breast) and liver diseases (such as viral hepatitis, metabolic factors) can help detecting diseases at a treatable stage, reducing long-term morbidity, mortality, and treatment costs. If there were no mechanisms for prepaying for them, however, households, especially those with lower incomes, would often postpone or skip preventive measures, thereby increasing the financial and health costs at the advanced stages of disease.

OOP and catastrophic health expenditure

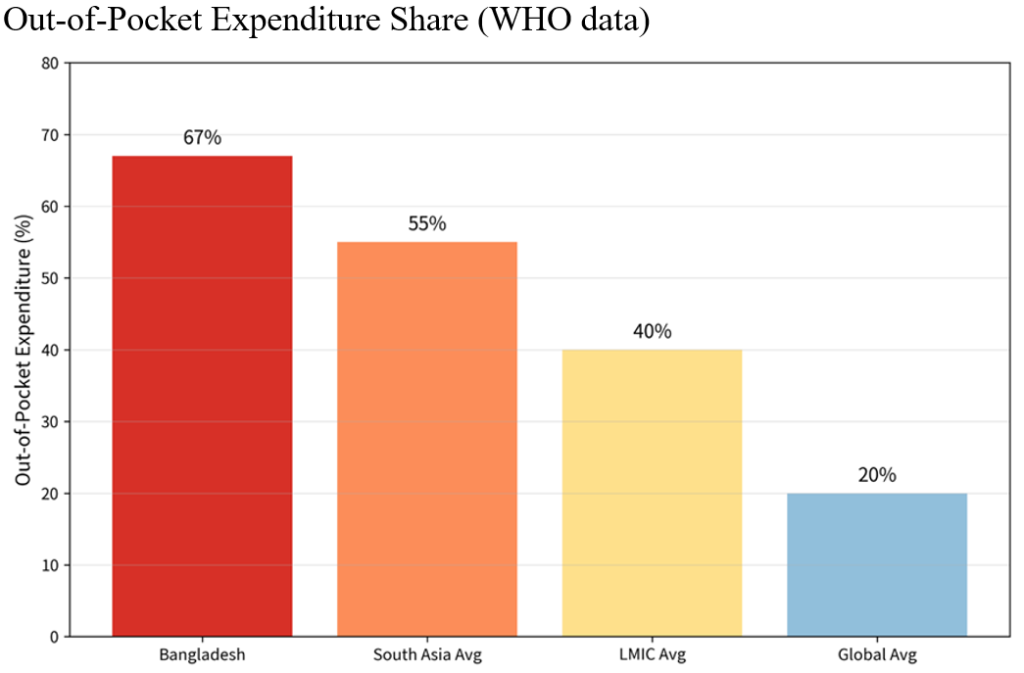

In Bangladesh, out of pocket (OOP) payments are estimated to be around 67%, and as high as 73% during some periods of health expenditure, one of the highest rates in the world. This translates into immediate financial insecurity. According to World Bank and national studies, catastrophic health expenditure (CHE) (defined as expenditure exceeding 10% of total expenditure or 40% of non-food expenditure) occurs in 10–25% of households, and is higher among poor, rural, and elderly households and those with chronic conditions.

Each year millions of people are pushed deeper into poverty by OOP. Medicines are the biggest component (around 60-64%) of OOP followed by hospital care and diagnostics. Households survive on credit, selling assets or cutting back on essential purchases, setting them up in long-term poverty traps. This creates a clear causal pathway to poverty and inequality: high OOP → financial risk → delayed care → poor health outcomes → increased future costs and inequality.

Each year millions of people are pushed deeper into poverty by OOP. Medicines are the biggest component (around 60-64%) of OOP followed by hospital care and diagnostics. Households survive on credit, selling assets or cutting back on essential purchases, setting them up in long-term poverty traps. This creates a clear causal pathway to poverty and inequality: high OOP → financial risk → delayed care → poor health outcomes → increased future costs and inequality.

One of the key factors of financial vulnerability is the high expenditure on medical care in private hospitals, which now provide most advanced and specialized medical treatment in Bangladesh. Public facilities are overcrowded, and medicines and equipment are scarce, while the fees charged by the private facilities are often much higher for consultations, diagnostics, surgeries and medicines. Limited trust or capacity in the public health services means many households, even those of middle income, must resort to private services for serious illnesses.

GHS Index and system vulnerability

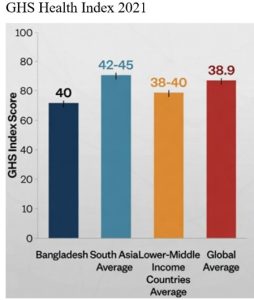

The Global Health Security Index (GHS Index) exposes structural vulnerabilities and Bangladesh’s overall score (around 40/100) indicates low levels of health system robustness, surge capacity, and overall health system resilience. These vulnerabilities are compounded by high OOP dependence, which reduces minimum population coverage and the system’s capacity to call on resources in the event of a crisis.

The Global Health Security Index (GHS Index) exposes structural vulnerabilities and Bangladesh’s overall score (around 40/100) indicates low levels of health system robustness, surge capacity, and overall health system resilience. These vulnerabilities are compounded by high OOP dependence, which reduces minimum population coverage and the system’s capacity to call on resources in the event of a crisis.

Case Study: Gonoshasthaya Kendra’s Health Insurance Scheme

A notable example of health insurance in Bangladesh is the community-based health insurance scheme developed by the Gonoshasthaya Kendra (GK). It started in the early 1970s when the community members used to get healthcare services for a standard rate of two taka. However, the GK recognized that equal payments from all households were inequitable, because the wealthiest households could contribute more than the poorer ones.

To address this issue, the organization gradually developed a socio-economic classification system based on household wealth and social status. Initially, beneficiaries were divided into three groups – rich, middle class and poor- but the system was later expanded to cover five groups: rich, upper middle class, lower middle class, poor and ultra-poor. Since 2012, an additional category has been introduced within the poor group, resulting in a six-tier classification system. The approach aimed to improve equity in healthcare financing by linking contributions to households’ socioeconomic conditions.

The scheme later evolved to address the healthcare needs of ready-made garment (RMG) workers. After the Rana Plaza collapse and Tazreen Fashions factory fire, financial protection of garment workers was identified as a key concern by the GK. After getting the support of development partners, a health insurance scheme was launched for the RMG workers. The scheme currently provides coverage for approximately 32,000 individuals, including workers and their family members, covering common illnesses, referral services, and basic healthcare support. Financial assistance is available up to a specified limit, while highly specialized treatments such as open-heart surgery and complex neurological procedures remain outside the coverage package.

According to a senior GK official, the experience demonstrates that health insurance is both feasible and necessary in Bangladesh. However, challenges related to financial sustainability remain, as current premium levels are often insufficient to cover healthcare costs. The GK model highlights the importance of equity-based financing, community participation, and financial risk protection. It also provides valuable lessons for Bangladesh as the country works toward Universal Health Coverage (UHC), emphasizing the need for strong governance, effective monitoring, and a bottom-up approach that reflects the needs of communities.

According to a senior GK official, the experience demonstrates that health insurance is both feasible and necessary in Bangladesh. However, challenges related to financial sustainability remain, as current premium levels are often insufficient to cover healthcare costs. The GK model highlights the importance of equity-based financing, community participation, and financial risk protection. It also provides valuable lessons for Bangladesh as the country works toward Universal Health Coverage (UHC), emphasizing the need for strong governance, effective monitoring, and a bottom-up approach that reflects the needs of communities.

Establishing a National Health Insurance System in Bangladesh: A feasible pathway

The preceding sections highlight the need for stronger financial risk protection in Bangladesh due to persistent health inequities, a growing burden of non-communicable diseases (NCDs), and high out-of-pocket (OOP) healthcare expenditure. The experience of Gonoshasthaya Kendra demonstrates that prepayment and risk pooling are feasible in the Bangladesh context. However, community-based health insurance schemes remain limited in scale and coverage, underscoring the need for a broader national approach. A national health insurance system should therefore be viewed not as a replacement for these initiatives, but as their gradual expansion and integration into a unified framework.

Bangladesh already possesses a policy foundation for health insurance through the Health Care Financing Strategy (HCFS) 2012–2032, which aims to reduce OOP expenditure and expand social health protection. As part of this strategy, the government introduced the Shasthyo Surokhsha Karmasuchi (SSK) in 2016, a tax-funded health protection scheme for below-poverty-line households. In addition, experiences from Gonoshasthaya Kendra, health insurance programmes for the RMG workers, healthcare benefits for government employees, and the country’s extensive network of community clinics and primary healthcare facilities provide important building blocks for future reform. These initiatives suggest that the pathway to national health insurance lies in strengthening, expanding, and integrating existing mechanisms rather than creating an entirely new system. Nevertheless, limited insurance coverage and low public investment in health remain major barriers to implementation.

International evidence and Bangladesh’s own strategy point to a sequenced “expansion model” built on five pillars.

- Political commitment and legislation: Every successful low- and middle-income country reform began with a binding legal mandate and a dedicated purchasing authority rather than a policy aspiration. Bangladesh would need a National Health Insurance Act establishing an autonomous national health insurance authority empowered to pool funds and purchase services.

- Resource mobilization that does not rely on premiums from the poor: The most important design lesson is that countries achieving genuine financial risk protection financed it largely through general taxation and earmarked levies, not contributions from the informal sector. Bangladesh could combine increased budgetary allocation with earmarked “sin” taxes on tobacco and sugary products, channelled into a single national health fund.

- A single risk pool and strategic purchasing: Fragmentation is the recurring failure mode. The purchaser of services should be separated from public providers, allowing the authority to buy care from both public and credentialed private facilities and to drive quality through contracts.

- Population segmentation with a subsidised core: Following SSK’s logic, the government should fully subsidize the below poverty line (BPL) population, cover formal-sector workers through payroll contributions, and progressively subsidize informal-sector households on an ability-to-pay basis.

- Provider-payment reform and digital administration: Closed-end mechanisms such as caps for outpatient care and case-based payments for inpatient care contain costs, while a digital claims-management system reduces leakage and builds the public trust that voluntary community-based health insurance (CBHI) in Bangladesh has historically lacked.

Lessons from Rwanda

Rwanda provides an important example for Bangladesh. Following the 1994 genocide, Rwanda expanded health coverage through its national community-based health insurance scheme, Mutuelles de Santé. Premiums were linked to households’ socioeconomic status, with the poorest populations receiving full government subsidies. Over time, the scheme achieved high levels of coverage, increased healthcare utilization, and reduced catastrophic health expenditure. Rwanda’s experience demonstrates that community-based insurance principles can be successfully scaled up to the national level when supported by strong government commitment, mandatory participation, and targeted financial protection for vulnerable groups. For Bangladesh, this experience reinforces the potential of building upon existing community-based initiatives such as the Gonoshasthaya Kendra model while ensuring state support for poor and disadvantaged populations.

Conclusion

Health insurance should be viewed not merely as a health-sector reform, but as a critical instrument for achieving Universal Health Coverage (UHC). Persistent health inequities, a growing burden of non-communicable diseases, and high out-of-pocket healthcare expenditure continue to limit equitable access to healthcare in Bangladesh. Experiences from the Gonoshasthaya Kendra and other emerging insurance initiatives demonstrate that risk pooling and prepayment mechanisms are feasible within the Bangladesh context. Moreover, existing policy frameworks and pilot programmes provide a foundation for broader reforms. The challenge is no longer whether financial risk protection is necessary, but how Bangladesh can translate fragmented initiatives into a coordinated national health insurance system that ensures equitable and affordable healthcare for all.

Sabiha Binta Siraj

Sabiha Binta Siraj is a final year student of Population of Public Health Sciences (PPHS) at the Department of Social Relations, East West University (EWU), Bangladesh. She has presented her research on menstrual health, loneliness, and mental health at three international conferences. An EWU merit scholarship and UTAship recipient, Sabiha is currently working on menopausal coping strategies among Bangladeshi women and knowledge, attitudes, and practices (KAP) of vaping among university students.